Cash flow and financial uncertainty are among the biggest sources of stress for many business owners, but they don’t have to be.

Cash flow projections are an incredibly important business tool that every business owner should know how to create and use. They allow you to look ahead, anticipate potential financial challenges and plan for your future growth with confidence.

In this article, we’ll break down exactly what cash flow projections are, why they’re so valuable and how you can create your first one.

What Is a Cash Flow Projection?

A cash flow projection consists of a forecast that predicts how much cash will come in and go out of your business over a future period of time.

It acts a bit like a roadmap that enables you to plan ahead, ensuring you don’t run out of cash and that your business remains liquid. If any potential issues are identified in the cash projection, you can take action before they become serious problems.

Cash flow projections are also great for expense planning and making informed decisions around hiring, investing and operational costs.

All cash flow projections consist of several core components:

- Cash inflows: The money coming into your business, such as customer payments, loans and tax refunds.

- Cash outflows: The money going out of your business, such as rent and utility bills, software subscriptions, staff wages and debt repayments.

- Timing: The time and date when money moves in or out of the business. A good projection matches inflows and outflows by date, so you can see the net cash flow for each period.

Cash flow projections can be generated for any time period, but the most common formats are:

- Weekly: Best suited for startups, seasonal businesses and rapid-growth businesses where cash is tight or unpredictable.

- Monthly: The most common period, used for more established businesses with steady growth.

- Quarterly: Better for long-term project planning and larger, more stable organizations.

Cash Flow Projection Versus Cash Flow Statement

Cash flow projections and cash flow statements are often confused, but they focus on different time periods, so it’s important to distinguish between them.

A cash flow statement shows what happened in the past. It’s based on historical records and is used for financial reporting, tax calculations and analysis.

In contrast, a cash flow projection looks ahead and shows what’s expected to happen. It’s based on estimates and anticipated payments, and it’s used primarily for planning and decision-making.

The two are linked in some ways, though.

You can use the cash flow statement to see how accurate your projections were. Conversely, the data generated from cash flow statements can help you make better cash flow projections.

Why Cash Flow Projections Are Important

Cash flow projections are not just for one type or size of business; they’re essential for every business. Here’s why they matter:

Helps with Planning Ahead

Planning is one of the main reasons businesses need cash projections. Without understanding how liquid you are likely to be a week or a month into the future, it’s much harder to make sound decisions or rectify issues.

For example, if a projection shows you’re likely to have a cash boost, you might plan to use that cash for larger expenses, such as equipment purchases or marketing campaigns.

However, if a low-revenue period is expected instead, you know you’re going to have to tighten your belt and dial back on spending until cash flow turns more in your favor.

Projections also enable you to spot any likely cash flow gaps and work out a plan before they turn into emergencies.

Informs Decisions

When you plan ahead, cash flow projections help you use current data to make shrewd decisions that won’t have negative consequences later down the line.

It’s the difference between making decisions based on hopeful long-shot targets and making them based on actual available cash. Using real data ensures your choices are realistic, not based on guesses or wishful thinking.

For instance, a projection will tell you if you can afford to hire a new employee next month or whether it’s best to wait a while. It can also tell you if you need to start negotiating better terms with suppliers to save money.

Supports Funding

If you need a larger cash injection, fundraising or applying for a loan is a typical route to take. However, any type of investor or lender will want to see how well you understand and manage your cash before they even think about approving you.

Solid projections build credibility and show that you’ve taken the time to do your homework. They also demonstrate that you will be able to reliably repay loans and manage investments.

Most lenders will ask for a 12-month cash flow projection, as well as historical data, since this gives them a fuller picture of how you operate.

If the numbers look good, you’re more likely to get approved. If the numbers are particularly strong, you’ll potentially be able to negotiate better terms.

Provides Business Insight

Cash flow is one of the most honest indicators of financial health. Even profitable businesses in a strong position can fail if their cash flow isn’t strong.

Projections give you valuable insight into how sustainable your business is in the present as well as in the future.

You can use projections to spot trends like rising costs or declining sales and put measures into place to remedy them. If cash flow is tight, your projection can help identify the cause so you can start working on a solution.

Lessens Your Stress

There’s no doubt that uncertainty breeds stress. Gaining clarity on what’s around the corner will help you sleep better at night.

When you understand what your cash flow is expected to do, you will feel more in control, even when things are less than ideal.

Cash flow projections are a proactive business tool that lets you preemptively prepare for situations. Without them, you’ll be forced to take a reactive approach and respond to things as they happen, which is infinitely more stressful.

How to Create a Cash Flow Projection

Cash flow projections may seem like another complicated financial task, but they’re actually quite simple to carry out. As long as you take the time to gather all the right information, it won’t take long before you have your first projection in hand.

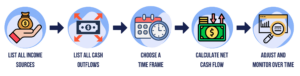

Here are the steps to create a cash flow projection:

Step 1: List All Income Sources

Your first job is to write a thorough list of all your business income sources. This is everything the business is expected to receive during the period you’re creating the projection for.

Common sources of income include:

- Sales revenue

- Recurring income like subscriptions and service plans

- Accounts receivable (invoices)

- Investments, grants or loans

- Other income like refunds, interest and royalties

Tip: Only include income that you reasonably expect to receive. Don’t count future sales or income if it is likely to fall outside the projection time frame.

Step 2: List All Cash Outflows

Next, list out all the cash that is likely to flow out of your business, including:

- Fixed costs like rent, insurance and payroll

- Variable costs like inventory and materials

- Operational expenses, such as advertising and utilities

- Loan and debt repayments

- Taxes

- Dividends

Tip: Check the last few months’ worth of bank and credit card statements to catch all recurring expenses.

Step 3: Choose a Time Frame

Pick the time frame that aligns most with your business needs:

- Weekly: For tight cash flow.

- Monthly: For balancing detail with ease. This is the most common time frame.

- Quarterly: For “big picture” planning.

- Custom: For specific use cases, such as investment seeking.

Step 4: Calculate Net Cash Flow

Calculating your net cash flow is easy. Simply subtract the projected outflows from the projected inflows, and that will tell you how much cash you have left over to play with. This is also referred to as your running cash balance.

Here’s the formula:

Inflows – Outflows = Net cash for the period

Step 5: Adjust and Monitor Over Time

Arguably, the hardest part of running projections is remembering to keep an eye on them over time.

Be sure to review your projections regularly and compare the projected running cash balance with the actual one. This will show you how accurate your predictions were and whether any adjustments are needed.

Remember, a cash flow projection is not a one-and-done thing. It’s a living document that is likely to change frequently as your revenue and bills grow and dip. Keep it updated and it will continue to serve you well.

To simplify the process, use technology. Spreadsheets, accounting software and dedicated projection tools can help you keep your projections updated and relevant.

Common Mistakes to Avoid

Even though it’s easy to learn how to do a cash flow projection, there are some common pitfalls that you must take care to avoid:

- Overestimating income: This is one of the most frequent mistakes that can cause a lot of problems, especially around overspending. Rely on realistic sales targets only.

- Forgetting variable and seasonal expenses: Missing these can make forecasts look healthier than they are, so review the previous years’ worth of expenses to identify irregular costs, as well as peaks and dips in sales.

- Not accounting for delays: Your cash flow is determined by when you get paid, not when the invoice is sent. Counting deals and invoices before they’re signed or confirmed can create cash flow shortages, even if sales look strong. Look at payment deadlines before including them in your projection.

- Not updating projections: Conditions change, clients delay things and new opportunities crop up. All of these will change the course of your projection, so don’t forget to keep it updated so it stays relevant to the current climate.

- Forgetting “invisible” cash: Some cash movements aren’t regular expenses but still affect your balance. Common “invisible” cash sources include loan repayments, owner withdrawals and purchases not marked as expenses. Even petty cash can contribute to this.

Tools & Templates

Although you can work out your cash flow projection using just pen and paper, it does help immensely to use a more specialized tool.

Basic, low-cost spreadsheet tools and templates are great for small businesses and freelancers who don’t typically use accounting apps or software.

Excel or Google Sheets are obvious choices, giving you good customization without any ongoing costs. You can easily find pre-formatted templates for these apps that will help you get started right away.

For more robust functionality, consider accounting software with built-in forecasting. Perfect for growing small and mid-sized businesses, QuickBooks Online and Xero both come with forecasting features. In addition, they link with your bank accounts and invoices to automate much of the process.

There are also dedicated forecasting tools like Float, Pulse and Futrli. These allow you to perform all types of financial forecasting and set up various scenarios. These tools typically integrate with accounting software and are best suited for larger businesses.

Finally, you have industry-specific tools. For instance, Lifetimely and BeProfit are specifically for Shopify sellers, while Bonsai is tailored to agencies and freelancers.

Our advice is to try out a few tools to see which suits you best. Most paid apps offer a free trial, so you can get started at no cost.

Examples of How Cash Flow Projections Work

To see how projections work in the real world, let’s take a look at a positive and a negative example.

Example of a Positive Cash Flow Projection

Let’s say you’re running a software and tech company.

Your inflows each month from direct sales and invoices are $275,000.

Your outflows each month from staff wages, subscriptions and operational costs are $230,000.

Therefore, your net cash flow would be calculated as $275,000 − $230,000, resulting in a cash flow projection of $45,000. Your company would have a healthy liquidity position and might be able to use that extra cash to help grow your company.

Example of a Negative Cash Flow Projection

Let’s say you’re running a business consultancy.

Your inflows each month from consultancy fees and contracts are $15,000.

Your outflows each month from hiring, training and operational costs are $20,000.

Therefore, your net cash flow would be calculated as $15,000 − $20,000, resulting in a cash flow projection of -$5,000.

Your company would currently be struggling with liquidity and should take some time to sit down and figure out areas to decrease outflows or increase inflows.

Get Professional Advice

Many companies struggle with projections and cash flow. The good news is, you don’t have to handle it alone.

That’s where Finvisor comes in. Our outsourced financial and back-office services are built for startups and small businesses, giving you expert-backed clarity and more time to focus on growth.

Reach out to Finvisor and get the expert financial backbone your business needs to thrive.

Let's chat

Get on our calendar for a free introductory call.Find out what it's like to work with Finvisor and how we can help you reach your business goals. Our financial advisors work hard for your business across our full suite of accounting and reporting services.

Request a Quote

We'll get back to you within a business day, usually sooner. Or you can schedule an introductory call and get on our calendar."*" indicates required fields