Audits are a process that no organization looks forward to. But as a business owner, you will likely experience one at some point, so it’s worth knowing what the process involves and how to prepare for one.

The key to successfully passing an accounting audit is staying informed about what audits are, how they work and what’s expected of you at each stage.

In this guide, you’ll learn what an audit involves, the different types and how to prepare your business for a smooth and successful process.

What Is an Accounting Audit?

Auditing in accounting is a formal evaluation of a company’s financial records conducted by professionals or certified public accountants.

These experts perform a deep review and examination to ensure the information presented is fair, accurate and in compliance with accounting standards.

All audits typically require your balance sheet, income statement and cash flow statement. Depending on the type of audit, other information may also be requested.

Internal vs. External Auditors

Audits can either be internal or external.

Internal auditing is performed by an organization’s own employees.

The main focus of these is to evaluate the existing internal controls and risk management policies. Essentially, they help prevent minor problems from escalating into bigger issues.

External audits are carried out by certified public accountants who are not affiliated with the organization in any way.

These auditors are thorough. By examining financial documents and testing internal controls, they can form an unbiased opinion on whether financial statements are accurate or misstated.

External audits can also be carried out by the IRS to verify tax returns. These are initiated by government officials and typically triggered by discrepancies in the organization’s reported income.

The Purpose of an Accounting Audit

The primary purpose of an audit is to confirm that an organization’s financial statements are accurate and free from discrepancies. It also ensures the organization’s accounting methods comply with applicable laws, regulations and accounting standards.

However, audits serve a greater purpose than just checking accuracy.

This process can uncover genuine errors, fraud incidents and gaps in internal controls. When these issues come to light, companies can take swift action to mitigate these risks.

Additionally, audits raise stakeholder confidence. This is important for reassuring shareholders and investors that the organization’s financial information is credible.

Beyond that, they increase transparency, which builds trust and holds employees accountable for financial activities and record-keeping.

Five Types of Audits

There are five main types of audits. Each serves a distinct objective and focuses on a specific area.

1. Financial Statement Audit

A financial statement audit investigates a company’s financial records and statements to determine whether they are complete, accurate and in compliance with Generally Accepted Accounting Principles (GAAP) and/or International Financial Reporting Standards (IFRS).

This audit is generally conducted by external auditors and provides an opinion on the reliability of the financial records.

All public US companies must undergo an annual financial audit to provide a full picture of their financial health and condition.

2. Internal Audit

As discussed above, internal audits are carried out by an organization’s own auditors (employed staff or hired contractors). They assess the effectiveness of risk management policies, operational procedures and internal controls.

The aim is to reduce risk by improving processes and identifying weaknesses so the organization is better prepared for an external audit. These audits help organizations run more efficiently.

3. Compliance Audit

Compliance audits determine whether an organization is following internal and external rules, standards and policies, as well as complying with regulations. Tax audits, for example, fall into this category.

These audits protect the organization from any noncompliance penalties and reputational damage by ensuring it adheres to the requirements.

4. Operational Audit

While financial audits focus on the numbers, operational audits scrutinize the efficiency of an organization’s operations and find ways to improve them. They often uncover issues in internal processes, strategic planning, goal management and other areas.

Operational audits are generally conducted by internal auditors, but it’s also possible for them to be carried out externally.

5. Forensic Audit

Forensic audits are required when an organization is suspected of theft, fraud or financial misconduct. They are conducted by a specialized external accounting team that carries out detailed examinations of financial records.

The goal is to gather evidence that can be used in legal proceedings or a court of law. Additionally, the auditor may be called to serve as a witness during any trial proceedings.

Forensic audits may also be called upon in other situations, such as disputes over bankruptcy or business closure.

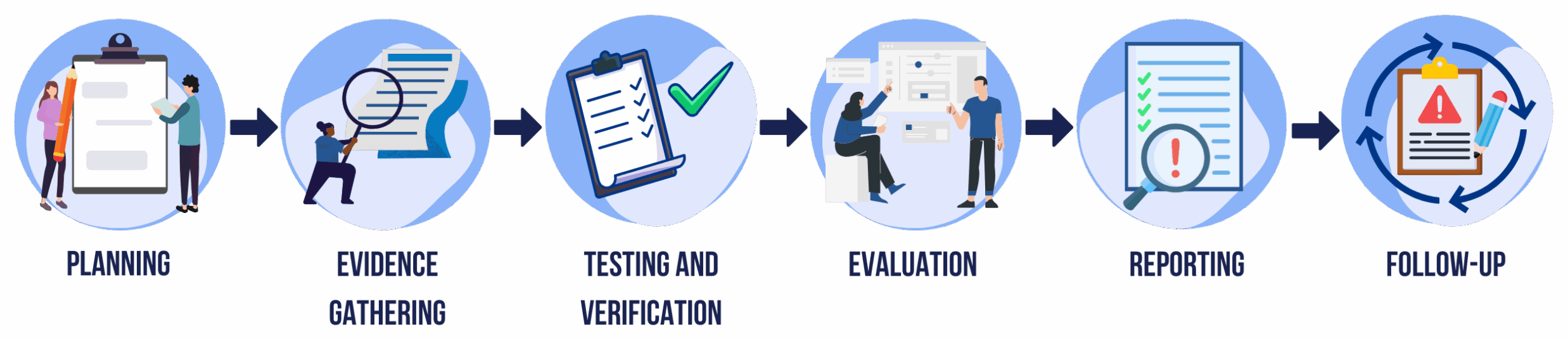

The Audit Process, Step by Step

Accounting and audit processes vary based on the audit’s complexity and the regulations specific to the industry or state jurisdiction.

However, these six steps will apply to any type of external audit.

1. Planning

First, the business will meet with the external auditor and go over the expectations and objectives of the audit. At this point, the auditor will:

- Gather information about the business, including its industry, regulatory environment and other relevant factors.

- Define the scope and strategy of the audit, including the timeline of what takes place and when.

- If needed, carry out a preliminary risk assessment to determine what audit efforts should focus on.

Once this process is complete, the auditor will create a detailed plan outlining the specific tests and procedures.

2. Evidence Gathering

During this stage, the organization is expected to comply and provide the requested documentation promptly. With the information in hand, the auditors will then:

- Inspect the documents and records.

- Look at tangible assets like inventory to confirm existence and condition.

- Observe business processes and activities to assess performance.

- Perform staff interviews to clarify facts.

- Request verification from relevant external bodies like banks and lenders.

- Verify repeating procedures and calculations to confirm they are accurate.

- Compare financial ratios and trends with historical data to identify risks or inconsistencies.

3. Testing and Verification

Once sufficient evidence has been obtained, the auditors will move on to test internal controls. This is to evaluate whether existing controls are functioning as intended and can detect irregularities or misstatements.

Auditors will also carry out substantive tests, such as tracing, vouching, comparisons and recalculations. These will verify that the financial statements provided are accurate and reliable.

Finally, statistical or judgmental sampling is used to select transactions and balances for testing.

If any irregularities are found during this process, they will be discussed with the organization for clarification.

4. Evaluation

Now the auditors have everything they need to make meaningful conclusions.

At this point, they will put together a full evaluation that includes:

- Any identified errors and misstatements, including their significance and impact on financial reporting.

- Whether the initial risk requires reassessment through additional audit procedures.

- An evaluation of internal controls to determine whether they are effective or if improvements are needed.

Before moving on to the next stage, auditors will typically gain written confirmation from management to confirm the accuracy of their findings.

5. Reporting

The formal audit report consists of all the findings, conclusions and recommendations, along with any identified issues and guidance on how they should be addressed.

The report is given to management for review, feedback and action plans based on the auditors’ recommendations.

Once the auditor has the response from management, the final report is compiled and distributed to the necessary stakeholders.

6. Follow-Up

After the final report has been issued, the organization is expected to follow through on any expected actions and improvements.

To verify this, the auditor will conduct follow-up sessions, ensuring that everything has been completed on time. Note that additional reports will be compiled and distributed as needed.

Depending on the audit’s outcomes, continuous monitoring may be implemented to ensure continuous improvement.

Audit Opinions and Outcomes

Part of the final audit report includes a professional opinion on the fairness and accuracy of the organization’s financial statements.

There are four main types of audit opinions:

- Unqualified (clean) opinion: This indicates that the auditor is satisfied that the financial statements are fairly presented and comply with regulations and accounting standards. This is the outcome that organizations want, because it signals that there are no major issues found.

- Qualified opinion: This is given when the auditor finds certain issues, like a deviation from accounting principles, but the financial statements are still fairly presented. It signals that, except for specific areas, the financial statements are found to be reliable.

- Adverse opinion: This is severe and indicates significantly misstated and untrue financial statements. Typically, an adverse opinion signals fraud or extreme mismanagement.

- Disclaimer of opinion: If the auditor is unable to obtain sufficient evidence to form an opinion, such as when records are missing or audit procedures cannot be performed, a disclaimer is issued. This signals that the auditor does not express any type of opinion and may trigger additional audits and investigations.

Standards and Regulations

Auditors must comply with both standards and regulations, which together establish a transparent framework for evaluating financial statements and internal controls. The main ones include:

- GAAP: A key set of rules used in accounting and other financial roles. They provide benchmarks and guidelines for how financial statements are prepared.

- Generally Accepted Auditing Standards (GAAS): A set of guidelines specifically for auditors containing three main categories:

- General standards that maintain professionalism, independence and objectivity

- Standards of field work that ensure proper audit planning and supervision

- Standards of reporting to ensure that reports are compiled in accordance with GAAP

- Public Company Accounting Oversight Board (PCAOB): Set of regulations that applies to audits for publicly traded US companies and includes detailed regulatory oversight.

- International Standards on Auditing (ISA): Global professional standards to ensure audits are performed consistently worldwide.

Each jurisdiction or country may also have its own regulatory standards, which means that organizations operating beyond its own state border will have to comply with them.

To simplify things, many countries align their national standards with the ISA. However, there are typically still some differences that must be observed.

How to Prepare for an Audit

Audit readiness involves focusing on several key areas. Here are some best practices you can put in place to ensure your organization is fully prepared.

Organize Records

The key area of preparation is the organization of financial records. Organizations must maintain clear records of any transactions, leases, insurance policies and loans.

Documents must be gathered and collated, ensuring each set is complete and accurate.

It is best practice to use document version control so there is an audit trail of who made changes to which documents and when.

Internal Controls

All internal controls must be reviewed and documented, and segregation of duties must be in place to mitigate errors and fraud. Additionally, companies should:

- Formalize approval processes and ensure they are applied consistently.

- Evaluate access controls to keep sensitive data secure.

- Use strong encryption protocols to secure data in transit.

Staff Readiness

Your staff need to be ready and prepared for the audit.

Inform them early in the process, train them on what to do and assign responsibilities to every team member so there is accountability.

Conduct self-assessments and pre-audit reviews to spot and remediate any issues before the audit begins.

Accounting Software

Your accounting software needs to be up-to-date. All transactions should be properly recorded and any outstanding reconciliations completed.

Be prepared to hand over access credentials to the auditors.

It’s best practice to use reliable accounting software because this minimizes many of the risks that auditors uncover.

Additionally, cloud-based software like QuickBooks or Xero is automatically updated, ensuring its workflows always comply with accounting standards and regulations.

Final Thoughts

If your organization’s finances are in order, there should be no reason to fear an audit.

In fact, it’s a good opportunity to look upon an audit as a way to strengthen your financial integrity even further. The more efficient and reliable your operations are, the more you raise your credibility.

If an audit has been requested and you feel stuck on what to do, it doesn’t hurt to get a financial expert on board.

At Finvisor, we provide outsourced certified accountants who will help you get your operations in order and successfully prepare for an audit.

Get in touch today to find out more.

Let's chat

Get on our calendar for a free introductory call.Find out what it's like to work with Finvisor and how we can help you reach your business goals. Our financial advisors work hard for your business across our full suite of accounting and reporting services.

Request a Quote

We'll get back to you within a business day, usually sooner. Or you can schedule an introductory call and get on our calendar."*" indicates required fields