When you’re running a small business, every dollar counts. That’s why many business owners seek out all available deductions and credits to lower the amount they owe during tax season.

Unfortunately, many small businesses don’t fully understand tax savings strategies, or are simply unaware of the credits and deductions they’re eligible for.

This knowledge can mean the difference between losing out on thousands of dollars or having the opportunity to reinvest that money back into the business.

To make sure you don’t miss out on crucial savings, this guide breaks down small business taxes, including what you need to know and how to plan accordingly.

Understanding Tax Basics

Before getting into the potential savings, it’s worth taking a moment to understand how small business taxes actually work.

Even if you rely on an accountant, having some basic tax knowledge enables you to have more productive conversations on how to structure things to minimize your tax burden.

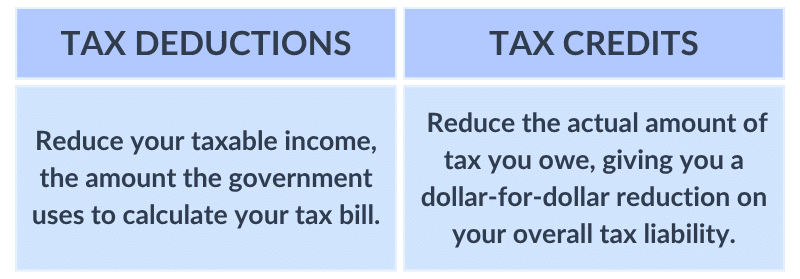

Deductions vs. Credits

First, let’s ensure you are familiar with how deductions and credits work.

Tax deductions, often called tax write-offs, reduce your taxable income, which is the amount the government uses to calculate your tax bill. More deductions mean you will pay tax on a lower amount of income.

For example, a tax deduction may reduce your income enough that you fall into a lower tax bracket, which would mean paying less tax overall.

Tax credits, on the other hand, reduce the actual amount of tax you owe, giving you a dollar-for-dollar reduction on your overall tax liability.

For instance, if you had a $50,000 tax bill and a $10,000 tax credit, you would end up only paying $40,000 in taxes.

How Income and Expenses Affect Your Tax Bill

Your income and expenses are used to calculate the total amount of tax owed.

This is calculated by subtracting legitimate business expenses from your total revenue. The remaining amount is what you’re taxed on.

Every deductible expense effectively lowers your tax bill. That’s why it’s so important to keep meticulous records of all your expenses.

However, you can only claim what you can back up with proof, so keeping copies of receipts, invoices and payment records is a must.

Common Tax Types for Small Businesses

Understanding the basics may seem simple, but you’ll need to keep on top of more than just one tax.

The type and amount of taxes your small business will need to pay depend on its size, structure and location:

- Income tax: Business owner taxes are based on your net profit. The rate depends on your business structure (S corp, C corp, LLC, sole proprietorship, etc.).

- Self-employment tax: Sole proprietors and partners must pay a tax on net earnings to cover social security, Medicare and unemployment.

- Estimated tax: Paid every quarter if you don’t have sufficient tax withheld from your income.

- Payroll and employment taxes: If you have employees, you must withhold and pay taxes on their wages.

- Sales tax: Applies to the sale of certain products, goods, services and industries.

Why Compliance Comes First

The IRS requires you to hold accurate and complete documentation of income, expenses and taxes, and to file everything on time.

If you file late, underreport or miss your estimated payments, you can land in hot water. Common consequences are accounting audits, financial penalties and, in the worst cases, criminal charges.

Any penalties your business receives can also damage your reputation and customer trust.

Key Small Business Tax Deductions

Now, let’s dive into the potential deductions your business can take advantage of.

Operating Expenses

Anything you pay to keep your business running (with the exception of labor) can be counted as an operational cost.

Common operational costs include:

- Monthly rent for business premises, like an office or warehouse

- Monthly rent for equipment

- Utilities, such as water, electricity and gas

- IT costs, like the internet and software subscriptions

- Office supplies, like stationery and printer ink

All expenses must be considered ordinary and necessary to your business. Even meals and travel expenses can be deducted if they were required for business purposes.

Employee-Related Costs

While you pay taxes on employee wages, they are also considered deductible. Other deductible employee costs include:

- Employee benefits like health insurance premiums

- Retirement plan contributions

- Bonuses and commissions

- Training costs

Home Office Deduction

If you work from home, you may qualify for a home office deduction. However, eligibility depends on whether you use the workspace regularly and exclusively for your business.

It works by deducting a portion of your rent or mortgage, utility costs and maintenance costs based on the size of your office relative to the size of your home.

The IRS simplified the deduction process in 2013 by offering an alternative option to an actual expense calculation. You may deduct $5 per square foot of office space, up to 300 square feet.

Vehicle and Mileage Deductions

Vehicles used for business purposes, like deliveries or traveling to meetings, can have a deduction applied.

Like home office expenses, you have two options:

- Calculate and deduct the actual expenses (fuel costs, repairs and maintenance), or

- Use a simplified, standard mile deduction (70¢ per mile in 2025)

Either option requires you to keep comprehensive logs of your mileage to qualify.

Startup Costs

Startups are in a unique position where they can deduct a portion of their startup expenses, as long as the total costs don’t exceed $50,000.

During your first year, you can deduct up to $5,000 for things like R&D, marketing and legal fees.

Any costs above $5,000 must be amortized (deducted in equal parts) and spread out over the subsequent 15 years.

Depreciation of Assets

Essentially, an asset’s resale value declines over time, and this depreciation can be deducted.

But depreciation can be a tricky concept to understand, especially when it comes to how you actually deduct it. Once again, you’ve got several different options:

- For larger assets like real estate, equipment, machinery and software, the IRS typically requires you to spread the cost deduction over the asset’s useful life.

- However, section 179 of the tax code allows you to deduct the full depreciation amount of qualifying assets in the first year (capped at $1.25 million in 2025).

If you choose to deduct depreciation over time, you’ll lower your tax bill for the subsequent years.

On the other hand, choosing to deduct the full value upfront frees up more cash that you can use to reinvest in your business, but it results in smaller deductions in subsequent years.

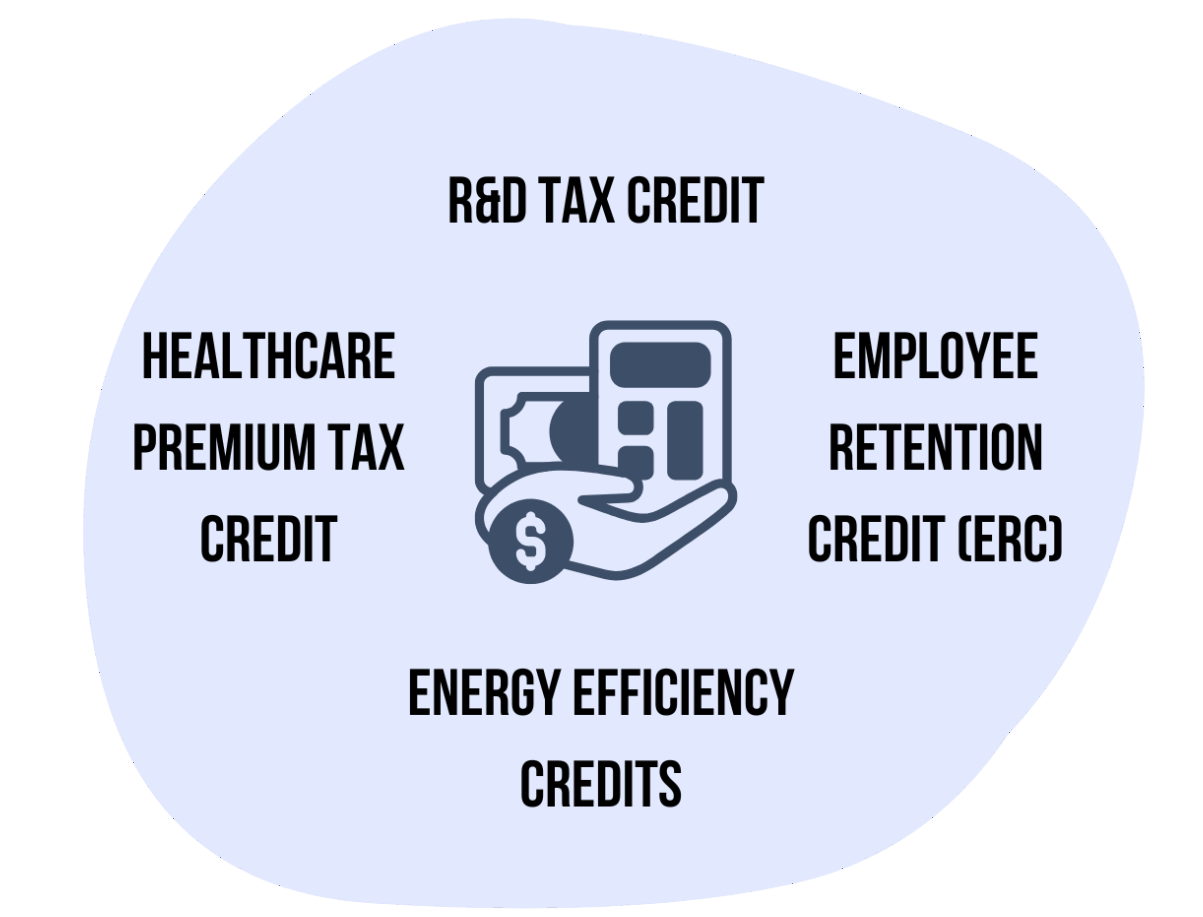

Small Business Tax Credits

The following small business tax credits can deliver substantial savings, as long as you meet the eligibility criteria.

R&D Tax Credit

If your business is developing new products, processes or software, or you’re working on technological improvements, then you may qualify for the R&D tax credit.

This allows you to claim up to 20% of qualified R&D expenses that exceed a base amount.

The base amount requires some complex calculations, so we recommend working with an accountant or financial expert to ensure you receive what you’re entitled to.

Employee Retention Credit (ERC)

The ERC rewards employers for retaining their employees through periods of economic downturn. This applies to businesses that suffer large revenue declines or are impacted by government shutdowns.

The total tax credit offered is up to $5,000 per employee for qualified wages.

Energy Efficiency Credits

If you invest in green energy initiatives, then a portion of the cost can be claimed back as a tax credit.

You can get up to 30% of the cost of installing solar, wind or zero-emissions energy systems on your business premises.

Various credits are also available for installing EV charging equipment, upgrading to energy-efficient HVAC systems and making qualified building improvements.

Healthcare Premium Tax Credit

You can get a healthcare premium tax credit if:

- You have fewer than 25 full-time employees

- The average salary is lower than $56,000

- You pay at least 50% of employee healthcare premiums

The credit is up to 50% of the premiums you (the employer) pay or up to 35% if you’re a nonprofit.

Strategic Tax Planning

Maximizing tax deductions and credits all comes down to how smart your tax planning strategies are.

To get these on point, we recommend doing the following:

- Stay organized by tracking your quarterly taxes to ensure you don’t miss a payment deadline.

- Work with a tax advisor year-round to help you make better financial decisions, such as timing major purchases or deciding when to expand.

- Integrate tax planning into your cash flow strategy. By accounting for tax payments and setting the money aside, you won’t be caught short in a critical moment.

Common Mistakes to Avoid

Another key aspect of smart tax planning is knowing the common mistakes that many small businesses make, so you can spot and rectify them before they become a problem.

In our experience, the top four errors we encounter most are:

- Omitting small deductions: Software subscriptions and office supplies may not cost a lot, but if you continuously forget them, they can add up to a significant amount over time. Document everything. Ideally, use a system that categorizes and tracks expenses automatically.

- Misclassifying workers: Always classify your employees correctly. If you mistakenly classify an employee as an independent contractor or vice versa, you can face penalties.

- Poor recordkeeping: Keep and store everything, including receipts, for at least three years. Use a proper filing system, and retain digital copies of all documents.

- Overlooking state-specific credits and incentives: Every state offers its own set of business credits. For instance, Colorado has a Work Opportunity Tax Credit, California has a credit for relocating to or remaining in the state, and New York has a credit for alcoholic beverage production. Be sure to research your state’s benefits so you don’t miss out on tax savings.

Tips for Maximizing Savings

Now that you know what’s deductible and what you can gain a credit for, here’s how to make the most of your savings:

- Use accounting software: QuickBooks and other similar software make it simple to track and record expenses automatically. You’ll not only be saving valuable time, but using automated software also ensures you won’t miss out on deductible transactions.

- Use your tax savings to reinvest in your business: Use it for marketing campaigns, upgrades, employee training or to pay down debts. This strategy will help your business grow and scale faster, setting you up for long-term success.

- Stay informed about current and upcoming tax laws: The rules change constantly. What was available last year might not be available the next, and new credits can be introduced at any time. Subscribe to the IRS for updates and meet with your tax advisor regularly to stay informed and plan for upcoming changes.

- Find industry-specific tax credits: Like state-specific tax savings, certain industries enjoy unique tax perks. For instance, there’s the FICA Tip Credit for restaurants and a credit for contractors who build energy-efficient homes. Learn what’s going on in your niche so you don’t miss out.

Consult Specialized Tax Professionals

Navigating tax savings isn’t for the faint-hearted, especially if you’re looking to find as many deductions and credits as possible.

As a final tip, we recommend hiring a tax professional who specializes in small businesses or your industry. You don’t even have to take on a full-time staff member for the job.

At Finvisor, we provide outsourced financial expertise at exactly the level of service you require. Whether it’s for ongoing accounting tasks, end-of-year planning, small business owner taxes or CFO advisory services, Finvisor will match you with the right professional.

Our job is to help you maximize tax savings and ensure you get exactly what you’re entitled to. Plus, we’ll assist you in completing the paperwork necessary to claim savings.

To understand more about Finvisor and the types of services we offer, please don’t hesitate to get in touch. Our job is to get your finances in order and set your business up for long-term success.

Let's chat

Get on our calendar for a free introductory call.Find out what it's like to work with Finvisor and how we can help you reach your business goals. Our financial advisors work hard for your business across our full suite of accounting and reporting services.

Request a Quote

We'll get back to you within a business day, usually sooner. Or you can schedule an introductory call and get on our calendar."*" indicates required fields